Between the consolidation of players and the rise of biosolutions, dive into the key transformations of a sector seeking economic sustainability.

The AgTech Ecosystem in a Turbulent Global Context

Between climate emergency, natural resource crisis, and economic pressure, agriculture must reinvent itself. In this context, agricultural technologies (AgTech or AgriTech) appear as one of the key levers to reconcile productivity and sustainability.

But faced with a contracting global market, how is France positioned? An analysis of a maturing ecosystem, between challenges and strategic opportunities.

The French AgriTech ecosystem is currently at a decisive turning point, marked by profound changes both globally and nationally. On a global scale, the AgFoodTech sector is experiencing a notable reduction in investments.

According to data from the latest AgFunder report published in early March 2025, the amounts invested in this sector have progressively decreased over several years. Thus, although a moderation of the decline was noted in 2024, one must go back to 2018 to find a similar level of investment.

This observation reflects an uncertain recovery, particularly for the upstream of the value chain, where investments fell from $10.4 billion in 2013 to $8.1 billion in 2024. Conversely, the mainstream and downstream segments (logistics, processing, sales) show signs of recovery, at relatively low rates.

Furthermore, all AgTech verticals have experienced a reduction in investments globally, including biosolutions, which were still leading investments with $1.9 billion invested in 2024, but showing a 12% decrease compared to 2023.

A phenomenon that does not go unnoticed is the decline of Novel Farming Systems: vertical farms, alternative proteins, or urban farms, which have seen a 53% drop in investments since 2023. The symbolic example of Ynsect, a French unicorn placed in receivership, illustrates the difficulties of the sector.

Are you developing an AgTech innovation?

Contact us to discuss its concrete deployment within our network of agricultural stakeholders.

The French AgriTech Market in 2025: The End of Innocence and the Advent of Pragmatism

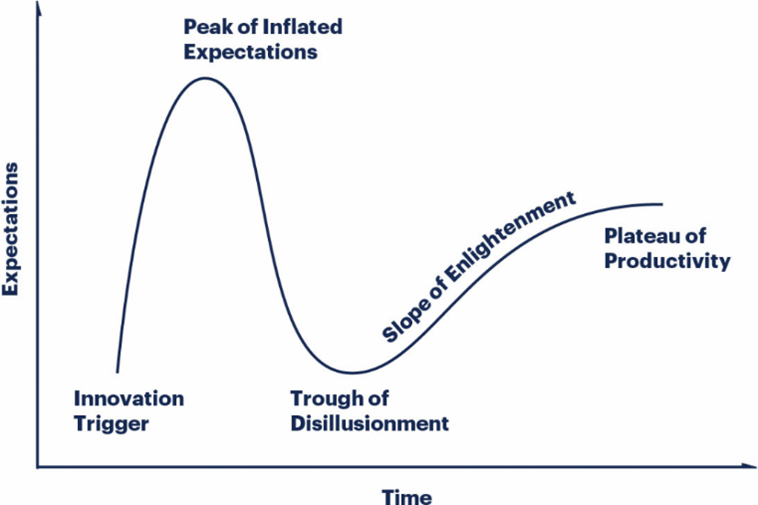

Nationally, AgriTech is characterized by a consolidation phase marked by contrasting funding dynamics. With €180 million raised in 2024 (-38.5% vs. 2023), French AgTech is not immune to the slowdown. But behind these figures lies a maturation dynamic, consistent with the Gartner curve applied to innovation.

After a phase of ‘peak of inflated expectations’ that saw sometimes excessive enthusiasm emerge in 2021-2022, the sector is now going through a period of disillusionment – the ‘trough of disillusionment’ – where technological promises clash with on-the-ground realities. Today, stakeholders seem to be initiating a tangible recovery; this marks the beginning of the ‘slope of enlightenment’, a stage during which innovative solutions begin to prove their real value and the profitability of their economic models. This maturation movement contributes to a consolidation of the ecosystem, oriented towards more prudent investments and a strategic approach focused on long-term viability.

However, this global context of decline masks some remarkable exceptions. Thus, the biosolutions sector stands out with €94 million raised, while robotics and automation also show slight progress, with €16 million raised.

This situation is partly explained by a shift in investment distribution. There has been a dramatic 70% drop in seed-stage funding for startups less than two years old, contrasting sharply with an explosion of investments in more mature companies, those aged 6 to 10 years, whose funding increased from €58 million to €204 million in one year, a rise of 254%.

This phenomenon reflects an increased investor preference for startups capable of demonstrating a solid business model, to the detriment of early-stage innovation. Furthermore, several acquisition and external growth operations, such as the mergers between Agryco and Farmitoo or between Isagri and Sencrop, indicate a trend towards sector consolidation.

In this context, the priority for players in 2025 will clearly be oriented towards profitability, a requirement confirmed by many entrepreneurs encountered in the aisles of the last International Agricultural Show in Paris, who insist on the need to control expenses and to find a viable economic balance to prepare for new fundraising rounds.

Biosolutions and Robotics: Two Pillars of the French Recovery

Two sectors are performing well in this global context: biosolutions and robotics. The biosolutions sector is emerging as a key lever for the agroecological transition. Indeed, this sector benefits from a rare alignment between regulatory expectations (Ecophyto plan), cooperative demand, and financial support.

The example of Elicit Plant and Micropep Technologies – which raised €45 million and €40 million respectively in 2024 – clearly illustrates the confidence placed in this sector, reinforced by the commitment of major industrial groups such as Bayer, UPL, FMC, and Syngenta, who are betting on open innovation, through partnerships or acquisitions of startups, to mark their presence in this promising sector.

In parallel, the field of robotics, automation, and machinery, although not yet experiencing an investment boom, shows steady growth, with global funding oscillating between $500 million and $700 million per year. In France, with €16 million raised in 2024, robotics is progressing modestly, but its strategic role is undeniable.

This sector, however, must address several regulatory, technological, and economic challenges. The transition to an industrial scale, essential to ensure the profitability of robotic solutions, represents one of the main stakes. In France, players like Naio Technologies and Aisprid – which raised €10 million in 2025 – illustrate this potential while addressing crucial issues such as reducing arduousness, adapting to labor shortages, and transitioning to precision agriculture.

Fermes Leader: Catalyst for Field-Anchored Innovation

In this rapidly changing environment, Fermes Leader positions itself as an essential partner for accelerating the deployment of AgriTech solutions.

By offering comprehensive strategic support, ranging from defining positioning to conducting pilots and concrete demonstrations with cooperatives and farmers, Fermes Leader facilitates the integration of innovations on the ground.

Its access to an extensive network of cooperatives allows startups to benefit from essential user feedback, thus adapting their solutions to the specificities of the French market. For entrepreneurs seeking acceleration and eager to transform current challenges into opportunities, Fermes Leader embodies the ideal partner for building a more sustainable, competitive, and resilient agriculture.

Our AgriTech Projects

Towards a Lean and Impact-Oriented AgriTech

While the French AgiTech ecosystem faces a decline in seed investments and a consolidation phase, the emergence of promising sectors like biosolutions and robotics offers promising prospects for the future. The pursuit of profitability, combined with a consolidation strategy, seems to be the key to overcoming current uncertainties and preparing the ground for tomorrow’s innovative agriculture.